The Litigation Network Value Chain

A Framework for Evaluating Litigation Networks

Harvest Strategy Group, Inc. (Harvest) is an accounts receivables management company celebrating its 10th anniversary in 2018. The requirements for running a litigation recovery program have changed dramatically over the last decade, with most of that change occurring within only the last four years, resulting in new requirements and responsibilities that are unfamiliar to many. This massive industry shift has upended the old value chain to create an entirely new set of considerations and economics that impact a creditor’s decision when selecting a litigation network partner. This paper will provide a framework for evaluating and selecting a litigation network using the value chain model as a guide.

Litigation networks bring value to creditors by offering a host of specialized services. For creditors who already have an outsourced litigation program, this article will be helpful in evaluating if you have right partner based on your unique needs. For creditors who are considering expanding or implementing a litigation program, each of these component values should be considered. If unaware of the recent industry changes, it’s easy to come to the wrong conclusion about the best solution.

Key Learnings

- The collection industry has changed dramatically in the last 10 years and especially over the last four years.

- Change will continue, driven primarily by CFPB enforcement actions, private law suits within the industry and states’ government rule changes.

- Industry Expertise and Vendor Audit/Oversight have become the #1 and #2 highest value services provided by litigation networks.

- The benefits of Service Consolidation, while still significant today, shifted from being the #1 value to the #7 value.

- The costs associated with operating a fully compliant litigation program have increased because the costs of running a non-compliant program have increased even more.

- The value that litigation networks bring to creditors has never been greater.

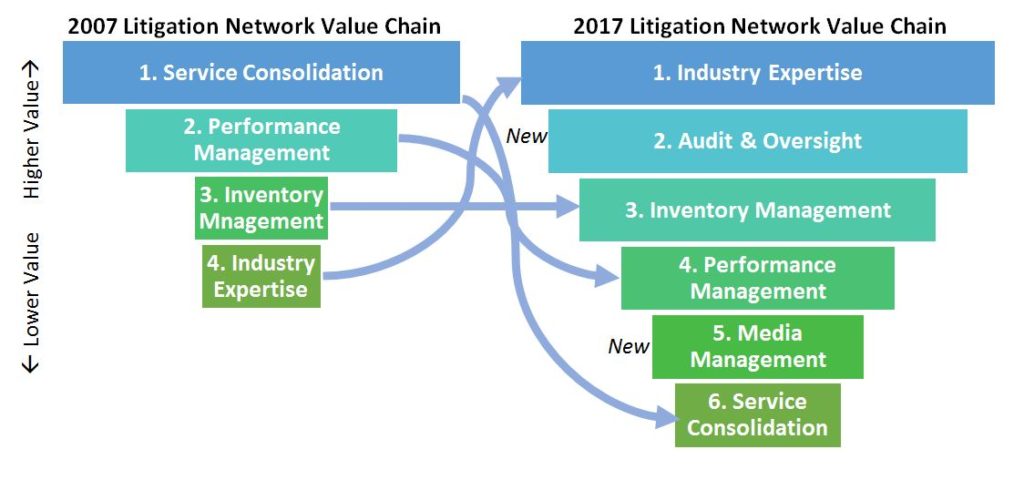

Below is a graphical comparison between 2007 and 2017 litigation network value chain. The sizes of the boxes represent the approximate value delivered to a creditor utilizing the services of a network. Each of the items in the boxes is discussed below.

What is a value chain?

The value chain is the reason that businesses exist. For example, as a simplified analogy, if you decide to build a house, you can do it yourself or hire a contractor. If you are serving as your own contractor, you are going to buy all the materials and hire and manage all the subcontractors (architect, framers, plumbers, electricians, painters, etc.) and hopefully finish on time and under budget. Alternatively, you could hire a contractor to handle the project. The contractor brings value because s/he has the relationships with the necessary subcontractors (saving time and improving quality), verifies insurance and licensing of those subcontractors (reducing risk), and has the knowledge of the process and required permits and inspections to make sure the project is done right and on time. Contractors bring value through established relationships, legal compliance and expertise.

2007 Litigation Network Value Chain

The 2007 value chain for litigation networks was based four powerful factors, all driven by simplifying the management process and maximizing recovery. It looked like this (ranked from greatest value to least value to a creditor):

- Service Consolidation

- Performance Management

- Inventory Management

- Industry Expertise

Each of the four values is explained below. In this article, we have not assigned a dollar value because the value varies by client and depends on many factors including: the type of accounts being handled, the level of existing infrastructure, the volume of accounts and the dispersion of those accounts across the United States. A creditor can estimate the value by assigning the cost of personnel required to support these activities and the resources required to build these systems.

1. Service Consolidation

This item refers to a whole host of benefits based on the fact that the litigation network operates as a single point of contact and has established relationships with collection law firms. Looking at the individual components, and the cost associated with each, it is easy to see why it used to be #1 value-generating feature. Service consolidation includes the following:

- The network has established contractual relationships with law firms, providing creditors with immediate access to the best individual law firms across the US.

- The network is responsible for proper insurance coverage, licensing, bar membership and trust account management, thus reducing risk.

- The network has established communication protocols with law firms for account placement, recalls, media, affidavits, disputes, status updates, remittances, cost bills, etc. Daily electronic updates for all activities performed on all accounts allows real-time monitoring and inventory management.

- The network provides consolidated status and activity reporting including a combined remittance and consolidated performance management and exception reports for improved decision-making.

- The network serves as the single point-of-contact for all issues, communications and coordination, greatly simplifying communication.

- The network is in the position of being an aggregator of inventory for many clients. This makes the network a larger client to the law firm than any individual creditor could be if placing accounts individually with law firms, thus increasing the level of attention on the accounts and the results.

2. Performance Management

The litigation network is responsible for recovery, and performance management refers to the activities that improve recovery results in a compliant way. Performance management activities include, but are not limited to overseeing law firm activities that generate recovery such as sending collection letters, making phone calls, filing suits, obtaining service, obtaining judgments and the filing of post judgment executions. Performance management also includes identifying accounts or groups of accounts where any of these activities are not in line with expectations and curing the situation. The cost of performance management is directly related to hiring individuals with this expertise and setting up the systems, reporting and processes to manage these activities across a portfolio. If this is ignored, recovery results will not be optimized.

3. Inventory Management

Inventory management is similar to performance management, but focuses those activities that relate to account management that do not necessarily produce recovery, but reduces risk. This includes all the activities related to accounts themselves to confirm that compliance related activities have occurred on time including: placing the accounts with the right law firm, recall accounts at the right time, handing disputes and fulfilling requests for documentation. The cost of inventory management is the cost of the individuals who perform these functions and the expertise required properly handling individual account level situation and the cost to develop the inventory management program for overall effectiveness.

4. Industry Expertise

The last value (ten years ago) was expertise within the litigation management arena. Filing suits against consumers across the United States requires a special knowledge base to operate with good results and minimum risk. It requires staff who have industry knowledge and direct experience with the specific type of account being litigated to make sure all the necessary information is communicated to the attorney so they can do their job in filing the lawsuit. Industry expertise also extends to the selection of the right law firms and the overall management and compliance of law firm activities. A lack of industry expertise will result in lower recovery and increased risk and legal exposure. The cost of industry expertise is related to the level of experience of the individuals who are hired to run the program and the salaries of those individuals.

In summary, the 2007 litigation network value chain offered significant value to the creditors in an industry that was primarily focused on efficiencies and recoveries. Those priorities have changed as explained next.

2017 Litigation Network Value Chain

Each of the items from the 2007 value chain exist today, but there are now additional items in the list and the order of items has changed. It looks like this:

- Industry Expertise (#4 in 2007)

- Audit & Oversight (new value)

- Inventory Management (#3 in 2007)

- Performance Management (#2 in 2007)

- Media Management (new value)

- Service Consolidation (#1 in 2007)

The order presented here is common in our experience except for performance management, which can rank higher or lower based on a creditor’s strategic priorities. For example, some creditors do not place any value on performance management because there is no amount of incremental recovery that can outweigh the cost of not being compliant. For others, compliance and recovery are of equal value. Each area is described in more detail below.

1. Industry Expertise

While industry expertise has always been a value of the litigation network model, it has risen to the #1 position because the complexity of the debt collection industry has increased dramatically in the last four years. This change cannot be overstated and the changes are expected to continue at a rapid pace. The Consumer Financial Protection Bureau (CFPB) was born from the Dodd Frank Wall Street Reform and Consumer Protection Act (Dodd Frank Act). Industry change is driven primarily by CFPB enforcement actions with large market players, private law suits within the industry and state government rule changes. Selected examples of CFPB enforcement actions which directly affect the debt collection industry are included in the references of this paper1. Below is a list of some of recent topics that have been the subject of enforcement:

- Guidelines for meaningful attorney involvement

- Requirements for original account level documents

- Proving account transfer and ownership

- Proving the balance due though authenticated business records

- Procedures for affidavit handling, review, signatory and notarization

- Requirements for affiant training and personal knowledge

- Prohibition against threatening legal action that the creditor does not intend to take

- Procedures for consumer complaint handling

- Requirements for third-party oversight

- Requirements for policies and procedures

- Guidelines for interest accrual practices

- Identification and cessation of unfair, deceptive or abusive acts and practices

- Notice requirements

- Consumer authentication requirements

In summary, expertise improves compliance and compliance reduces risk. This is the number one value added by litigation networks in today’s environment. Insourcing litigation network management expertise can be costly and take time. An adage sums up the cost of this item: “If you think the cost of compliance is high, you should see the cost of non-compliance.”

2. Audit/Oversight

While there has always been vendor audit and oversight, the Dodd Frank Act requirements as enforced by the CFPB increased the scope of audit requirements and thus the value of audit and oversight services to creditors, making vendor audit/oversight the #2 item in the value chain. The CFPB makes it clear that financial institutions can outsource services to third parties but cannot outsource the liability for those services because they have a responsibility for the compliance of those entities. The CFPB addressed in in its document titled: Compliance Bulletin and Policy Guidance; 2016-022, Service Providers, which read in part:

The CFPB recognizes that the use of service providers is often an appropriate business decision for supervised banks and nonbanks. Supervised banks and nonbanks may outsource certain functions to service providers due to resource constraints, use service providers to develop and market additional products or services, or rely on expertise from service providers that would not otherwise be available without significant investment. However, the mere fact that a supervised bank or nonbank enters into a business relationship with a service provider does not absolve the supervised bank or nonbank of responsibility for complying with Federal consumer financial law to avoid consumer harm.

In response to this shared responsibility for oversight, Harvest offers an industry leading, best in class, vendor audit and oversight program covering all Harvest vendors that is transparent to clients so they can see the standards, expectations and audit results. Clients can also participate with the Harvest auditor in the on-site audit. The program gives clients line-of-sight to law firm activities and compliance protocols and copies of audit results are freely provided to Harvest clients.

This item is linked closely to #1 Industry Expertise because it takes a high level of industry expertise to design, implement and manage a robust audit program. The program is not static and must continue to evolve in response to the industry. The cost of operating an audit program is significant and includes hiring experienced individuals (program managers and auditors with subject matter expertise) and travel costs for on-site audits. In our experience, one auditor can audit 3 to 5 law firms/agencies/vendors a month on average.

3. Inventory Management

The requirements for effective inventory management have evolved because of industry changes. Today, litigation networks are designed to not only track the same events as 10 years ago, but many more specific account level situations to ensure each situation is properly handled including but not limited to the following:

- Customer complaint tracking and response management

- Resolution of disputes and consumer claims of fraud and requests for validation

- Account balance validation and discrepancy resolution

- Requests for cease & desist

- Consumers represented by an attorney or other legal representatives

- Accommodations for non-English speaking consumers

- Proper authentication for consumer communication

- And others

Effective inventory management requires competent and compliant law firms and effective communication between the client and litigation network and the law firm handling the account. The cost of effective inventory management is making sure the entire process is designed and manage so that each account is handled correctly every time a compliance-relates situation arises.

4. Performance Management

It may seem obvious that a litigation network manages performance, but the truth is that among litigation networks, the entire gambit of options is available in the marketplace from those that offer no performance management to those that offer sophisticated performance management disciplines (such is the case with Harvest) to those in the middle. In 2007 this was the #2 highest value. The reason it has dropped in position is because of the risks associated with items #1 through #3; there is no amount of recovery that can offset the cost of running a non-compliant program. The costs are just too high. Proper performance management maximizes recovery results within the boundaries of operating a fully compliant program that is in compliance with all laws and regulations with a focus on consumer impact to avoid any activity that could be perceived as unfair or deceptive.

5. Media Management

Account documentation has always been part of the litigation process, but the CFPB enforcement action against Frederick J Hanna & Assoc3 brought Original Account Level Documentation (OALD) to the forefront of the litigation process and changed the way it is managed. As a result, effective media management must be a core competency of anyone managing a litigation program. The value of this function is substantial because OALD must be reviewed by attorneys for each case before sending the initial demand letter. Thus, without the proper documentation (even one missing document) the litigation process cannot start. To meet this requirement, the following steps must be performed:

- Identify which specific documents are required for filing suit (based on jurisdiction and account type);

- Identify if those documents exist within the creditors systems and retrieve them;

- Transmit those documents to the law firm with the placement of the account for their review.

These steps may sound simple, but in practice it can be a challenging process. For example, Harvest has developed a custom document management system which determines the minimum required documents based on the type of account (as determined by the local attorneys). The system reconciles the documents provided by the creditor to confirm all required documents have been received, securely delivers those documents to attorneys with the placement of the account and manages the request for any additional documents that may be needed after placement of the account.

6. Service Consolidation

The value of service consolidation (#1 in 2007) continues to be an important benefit of litigation networks today with all the same benefits as described earlier. The value of these benefits has fallen to the #6 position not because the value is less than before, but because the value of all the other components have increased.

Conclusion

Each of the components of the value chain should be considered to select the right litigation network. Making this decision used to be easier because the value chain was simpler and the primary value provided was service consolidation. Today’s requirements for expertise, audit, oversight, inventory management, performance management and document management make the process more complex and more valuable than ever before. Any litigation program must have these areas covered with a robust and evolving program that is responsive to industry developments. The value that litigation networks bring to creditors has never been greater.

REFERENCES

1 Following are examples of CFPB enforcement actions that have shaped the debt collection industry.

- September 18, 2017: National Collegiate Student Loan Trusts and Transworld Systems: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/national-collegiate-student-loan-trusts-and-transworld-systems-inc/

- January 9, 2017: Works & Lentz: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/works-lentz-inc/

- April 25, 2016: Pressler & Pressler: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/pressler-pressler-llp-sheldon-h-pressler-and-gerard-j-felt/

- February 23, 2016: Faloni & Associates: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/faloni-associates/

- September 9, 2015: Encore Capital Group: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/encore/

- September 9, 2015: Portfolio Recovery Associates: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/portfolio-recovery-associates/

- July 14, 2014, CFPB Consent Order Against Frederick J Hanna & Associates: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/frederick-hanna-associates/

2 CFPB Compliance Bulletin and Policy Guidance; 2016-02 http://files.consumerfinance.gov/f/documents/102016_cfpb_OfficialGuidanceServiceProviderBulletin.pdf

3 July 14, 2014, CFPB Consent Order Against Frederick J Hanna & Associates: https://www.consumerfinance.gov/policy-compliance/enforcement/actions/frederick-hanna-associates/